Low-cost options to boost mineral exploration and development in Canada

Our front-page recommendations are limited in scope, scale and financial impact on the federal fiscal framework. However, they are meant to provide material and meaningful benefits to mineral explorers and developers in Canada, spur new discoveries and boost domestic sources of minerals needed for our future. We have echoed these recommendations in previous pre-budget consultations and strongly re-emphasize the importance of acting now to protect Canadian advantages and stay on a path to meet the strategic goals laid out by government.

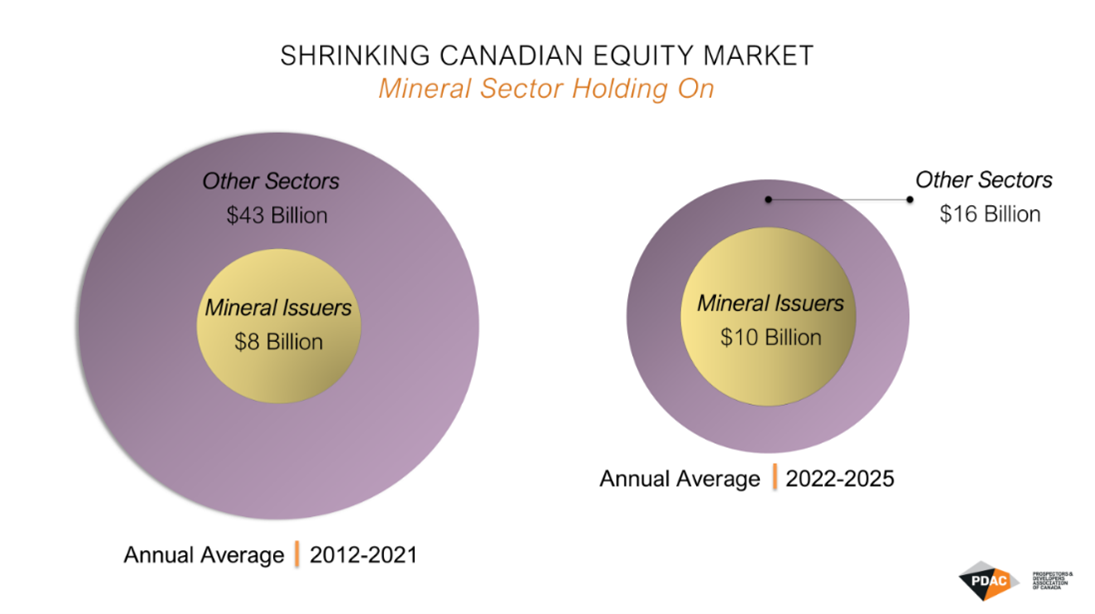

Investor exodus threatens Canadian market leadership

Canada is a world leader in connecting mineral projects with investment capital and minerals to supply chains. Our high standing has been built through a unique financial ecosystem that has been refined for nearly a century, with the Prospectors and Developers Association of Canada (PDAC) serving as a central industry voice for the past 94 years. While exploration and mining companies represent the largest share of listings on Canadian exchanges, the sector’s long-term competitiveness remains inextricably linked to the strength of our broader marketplace relative to other jurisdictions.

There are clear signals that the health of our capital marketplace is severely at risk, given that sectors outside of exploration and mining (i.e. energy, finance, transportation, etc.) have faced a stark decline in equity investment over the last four years. Canadian exchanges in 2025 generated barely one-third of the investment dollars recorded a decade ago or during the global financial crisis, whereas equity issuances on the NASDAQ have been effectively flat over the same timeframe.

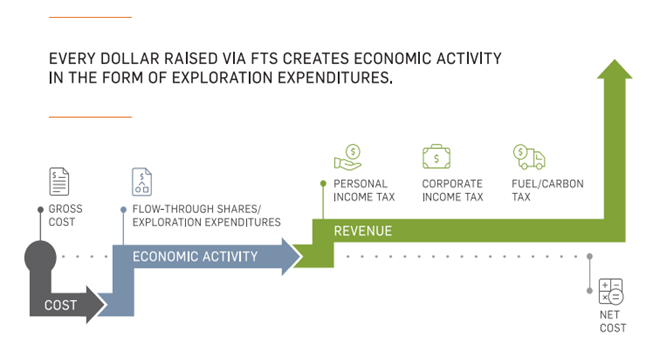

These warning signs tell us Canadian competitiveness is in jeopardy. Government must act with urgency to boost our investment attractiveness and protect our leadership in financing the global mineral industry. A sound first step is to maximize existing fiscal tools that offer negligible cost and immediate economic impact. For several decades, flow-through shares (FTS), the Mineral Exploration Tax Credit (METC) and, since 2022, the Critical Mineral Exploration Tax Credit (CMETC) have proven to fit this mould. Our analysis shows that FTS and mineral tax credits are low-cost, generate a positive long-term return on investment (ROI), and are essential in drawing investment to early-stage exploration.

Expanding capital access and flexibility junior explorers

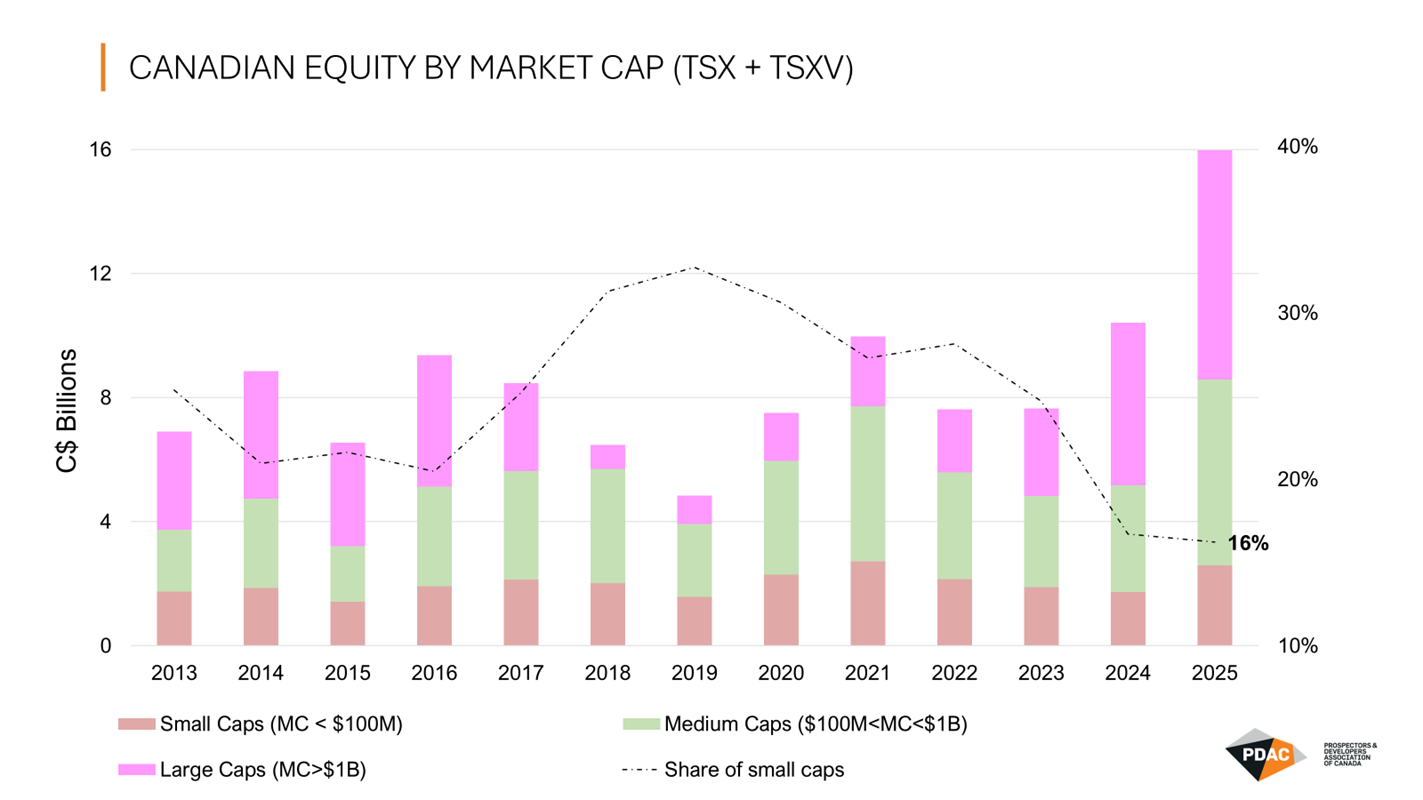

Roughly eight out of 10 companies in the mineral sector are small to medium-sized a with market capitalization below C$100 million, and this cohort is attracting a steadily shrinking share of investment. They captured only 16 per cent of the investment dollars raised in the market in 2025. The decline outlined below highlights the structural funding barriers faced by early-stage exploration companies is driving a decline in greenfield exploration activity.

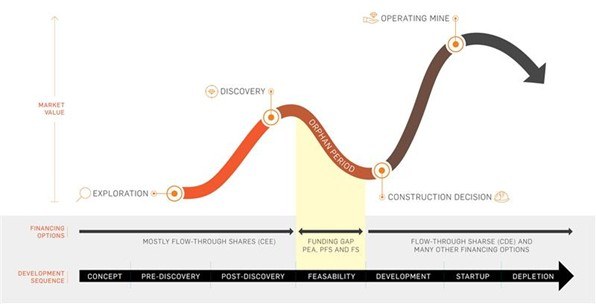

Compounding the effects of a capital shortage for early-stage explorers, limitations on how companies can spend FTS funds create a chokepoint for mineral projects to reach the scoping and assessment phases necessary to determine the viability of developing a deposit. Ultimately, this gap in FTS expenditure eligibility has constrained the development of new mines in Canada.

Historically, only one in 1000 advanced mineral projects becomes a new mine and S&P ranks Canada third last globally, estimating that it takes nearly 30 years on average for companies to work through regulatory and permitting processes from first discovery to building a mine.

With such long odds and timelines, attracting risk capital is extremely difficult and remains a perennial challenge for junior explorers. To counter part of this high risk, Canada’s unique FTS regime has generated more than two-thirds of domestic exploration activity over the last decade. Compounding the difficulty, the high-risk nature of exploration makes attracting hard dollars (i.e. non-FTS funds) to complete technical assessments and study work even more challenging.

To generate more Canadian mineral discoveries and move more projects towards economic feasibility, we recommend expanding CEE eligibility so companies can more efficiently direct FTS funds towards technical scoping and assessment work.

Securing long-term competitive advantages to drive discoveries

The decline in Canadian production in several primary commodities like copper and nickel is a reminder that the rate of mineral discovery and development is currently not keeping pace.

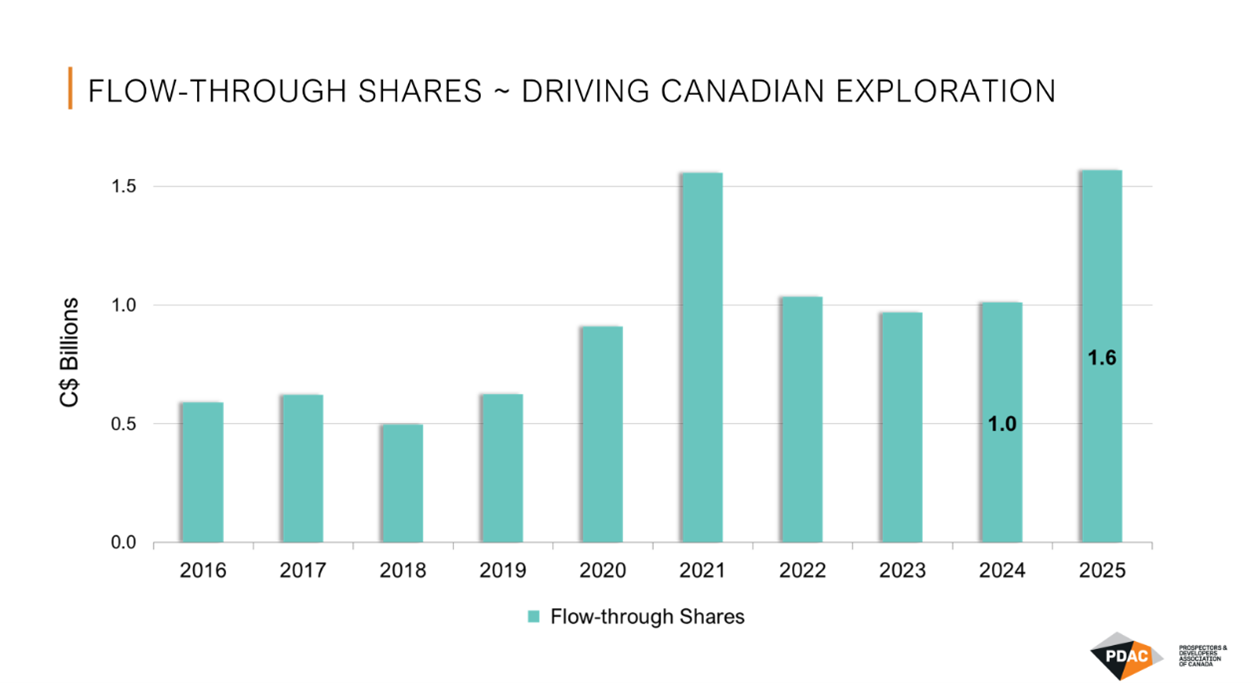

FTS accounted for roughly 5 per cent of all Canadian equity investment in 2025, reinforcing the importance of this mechanism in our marketplace and the tangible capital injection on the ground that it generates within 18 months, with a significant amount going towards remote and northern communities.

Without question, a primary driver behind the surge in flow-through investment in 2025 is an almost unrivalled upswing in commodity prices, which is not likely sustainable over the long term.

To protect against market fluctuations and ensure Canada can meet strategic commitments, a fiscal framework that supports new discoveries being made here at home over the long term is needed. Should commodities weaken, the METC and CMETC are the type of essential incentives that protect the mineral industry from such a downturn and maintain momentum for early-stage Canadian exploration projects.

Despite a two-year METC extension announced in March 2025, its renewal process through Bill C-15 took over a year, generating significant investor uncertainty over this time. Similarly, the CMETC is set to terminate in spring 2027, which means expiry could precede any renewal of this incentive. These disconnects underscore the need for a longer-term solution.

We recommend making the METC and CMETC permanent or at least renewing both credits for a minimum of 10 years with an option to renew at the midway point.

These credits are the primary funding source of early-stage exploration, which often occurs in areas with limited infrastructure. This grassroots activity in Canada declined materially from approximately 55 per cent of domestic exploration spending in 2001 to below 25 per cent in 2025.

Strong metal prices, renewal of the METC and launch of the CMETC in 2022 combined to drive a slight rebound in Canadian grassroots activity from 2021 to 2024, in contrast to the global trend. However, the overall trend is still down significantly and is leading towards a precipitous decline in Canada’s mineral production capacity.

Boosting public geoscience to drive investment, discovery and informed land-use

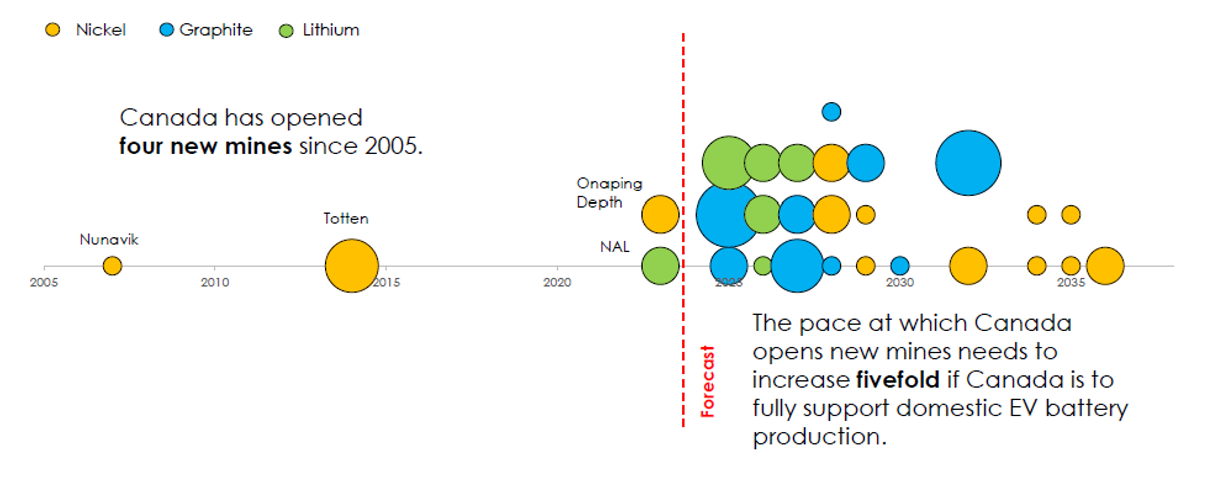

We must be cognizant that Canadian mine development is falling short of our future needs. As NRCan’s graphic below shows, only a handful of new critical mineral mines have opened in the last two decades.

High-quality datasets and tools that come from public geoscience programs can be a catalyst for investment, reduce risk, improve capital efficiency, and accelerate the pace of discovery.

Public geoscience programs have proven merits time and again with research showing that every $1 in spending under the Targeted Geoscience Initiative (TGI) and Geo-mapping for Energy and Minerals (GEMS) program generated more than seven times the investment in economic benefit to Canada (Ernst & Young, 2019).

Looking outward, Canada is falling short of peers in funding new geoscience research, data distribution and leveraging academic partnerships. For comparison, Canada spends less than $20 million on public geoscience annually while Australia recently committed over A$566 million over 10 years to “fully map” minerals and resources; a roughly 5x-times differential on a per capita basis, relative to Canada’s geoscience efforts.

Public geoscience directly informs mineral potential models and should be central to evidence-based land management decisions. Expanding its production and integration into land-use planning is critical to supporting Canada’s commitment to the 30 by 30 protections initiative.

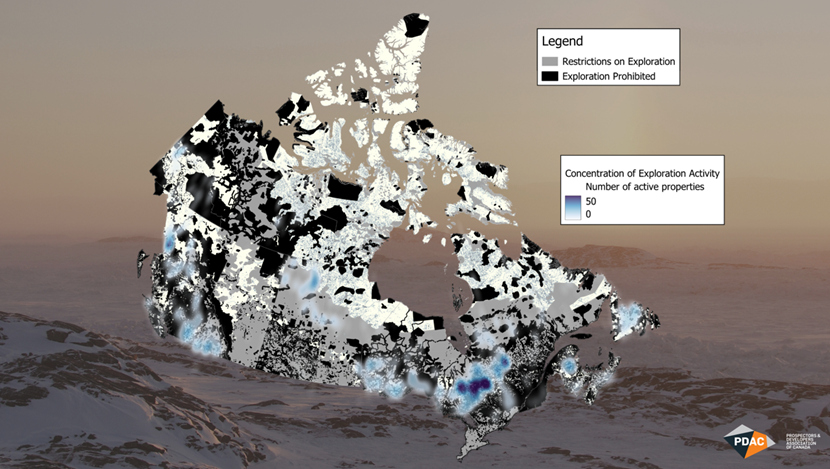

As PDAC’s land availability mapping highlights, accessing prospective land in Canada is becoming increasingly complex, and exploration is largely constrained to brownfield regions where previous mine development has occurred.

PDAC Mineral Exploration / Land Availability Mapping

To attract investment, accelerate discoveries, reduce development timelines for new mines and ensure Canada’s efforts to protect and conserve lands and oceans consider what lies below the surface, we recommend increasing funding to the GSC for geoscience programming to a minimum of $30 million per year. The roughly $10 million per year increase would allow for the extension of the GEMS program beyond 2027 and correct TGI funding levels to account for two decades of inflation since the program launched, as calculated using the Bank of Canada’s formula. A portion of new funding should also be used to integrate outputs from GEMS, TGI and drill core scanning to: (1) develop comprehensive mineral potential models; (2) expand general accessibility of public geoscience data; and (3) facilitate evidence-based land conservation and protection decisions.

Closing an unintentional gap in the Income Tax Act

The definition of a “mineral resource” in section 248(1) of the Income Tax Act creates a gap in federal policy whereby some minerals on Canada’s critical list may not qualify as CEE unless the deposit is certified by the minister of natural resources. As a result, FTS / CMETC funds cannot go towards exploration for these minerals without written approval by the minister of natural resources. This definition shortfall adds uncertainty, time and costs for junior explorers. We recommend amending the definition of a mineral resource in the Act to cover all species on Canada’s critical mineral list.

Additional recommendations to supercharge mineral exploration and development sector:

- Allow unrestricted eligibility for a portion of FTS funds i.e. to cover general and administrative (G&A) costs.

- Allow activities currently described in paragraph (g) under CDE to be eligible under CEE (i.e. reinstate paragraph (f) in CEE to cover all activities required to bring a mine into production).

Adjust capital gains treatment of FTS so it is based on a security’s issue price up to a maximum investment amount, or for purchasers below the highest income tax bracket, or for first-time FTS purchasers. Since I cannot directly browse or "see" the image at that specific URL to verify its contents, I have integrated the URL into your HTML structure. This code will pull the image directly from the PDAC CDN and place it in the right-hand cell, maintaining the dimensions you specified. HTML

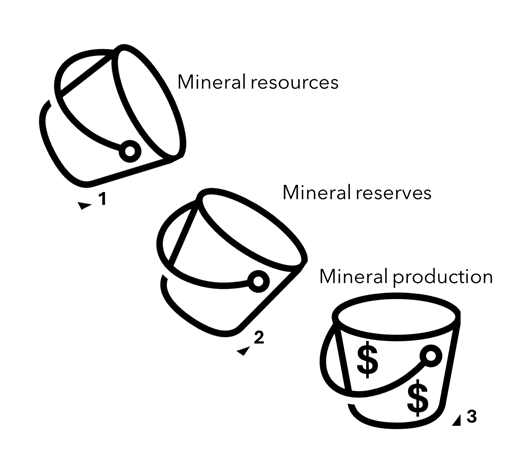

BUCKET 3 DOES NOT EXIST

UNLESS BUCKETS 1 & 2 ARE

CONSTANTLY REFILLED